August Orange County Housing Market Update

Orange County Market Update by the Numbers

Demand is down by 3% since the start of July, however over the last two weeks we have seen demand increase a little bit which is mainly due to the interest rate decrease we have seen over the last month.

Supply is up 6% since the beginning of July, most of that increase happened over the first two weeks of the month and over the last two weeks homes hitting the market have slowed down a bit.

Interest rates are current averaging 2.8%, down from 3% where they were at the beginning of July

The average days on market for a home in Orange County right now is 27 days, compared to the 5 year average of around 78 days for July you can see this market is still a deep seller’s market. In fact anything under 60 days is considered a seller’s market.

Foreclosure/Forbearance Data

With the foreclosure moratorium lifting, a lot of news articles have been circulating the internet predicting doom and gloom for the housing market. Let’s take a look at the actual data to determine how likely it will be that these eventual foreclosures will have a large impact on the housing market.

We currently have around 1.75 million homeowners still in forbearance programs. Out of the homeowners that have come out of forbearance from June through mid-July, only about 16% of them exited without a loss mitigation plan worked out with their bank. The rest have either paid missed payments back in full, paid off their home completely, sold their home already, or have worked out some type of loan modification with the bank to keep their home. So what about the rest that are still in forbearance? Let’s look at what we know about these 1.75 million homeowners.

Based on the current data we have about the homeowners that are still currently in forbearance most economists are estimating that somewhere between 10-20% of those will ultimately end up having to sell their home because they can’t financially afford to keep it. That will end up being somewhere between 175,000-350,000. Just to put that into perspective, during the last housing crash we had about 9.3 million foreclosures. Also, the average number of foreclosures that hit the market each year during the 3 years leading up the 2020 was around 290,260. As you can already see, this “wave of foreclosures” that you keep reading about will be no where near the numbers we saw during the great recession which caused housing prices to tumble. Even if 100% of those currently in forbearance ended up in foreclosures, we aren’t looking at numbers anywhere close to 9.3 million, in fact the numbers we will most likely see will not be that far above the amount we saw in a normal year leading up to the pandemic.

So why are economist predicting such a low number of foreclosures? There are a few main reasons.

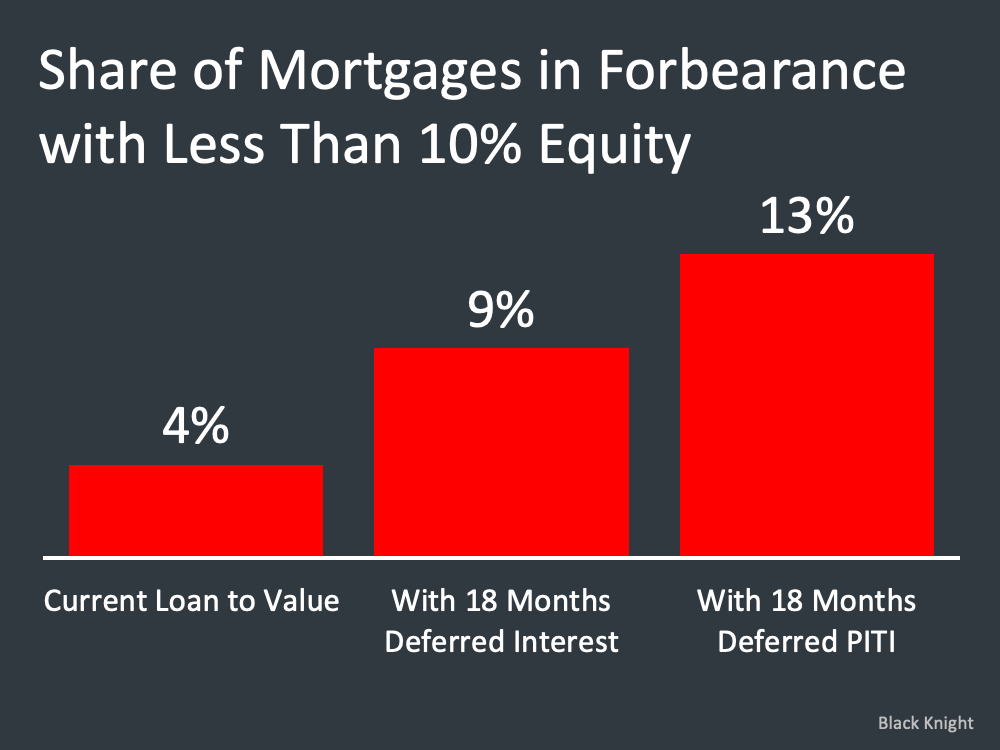

- Right now, according to Core Logic, Americans have more equity in their homes than every before, an average of $216,000. In fact, right now 96% of homeowners in forbearance currently have at least 10% equity in their homes. But you might ask, “Well if homeowners haven’t been making their monthly mortgage payments for the last 18 months do they really have at least 10% equity in their home?” This is a good question because that will give us a much more accurate real world idea of how many owners might be underwater on their mortgages. Luckily, Black Knight a leading mortgage data analysis company has calculated these numbers and they are estimating that even after taking into account missed payments when looking at total home equity, about 87% of homeowners still have more than 10% equity in their homes. I keep referring to this 10% number because if homeowners can’t make their payments and have at least 10% equity in their home, they can actually just go through the normal process of selling their home and avoid foreclosure entirely because they have enough equity to either make money on the sale of their home or at very worst break even.

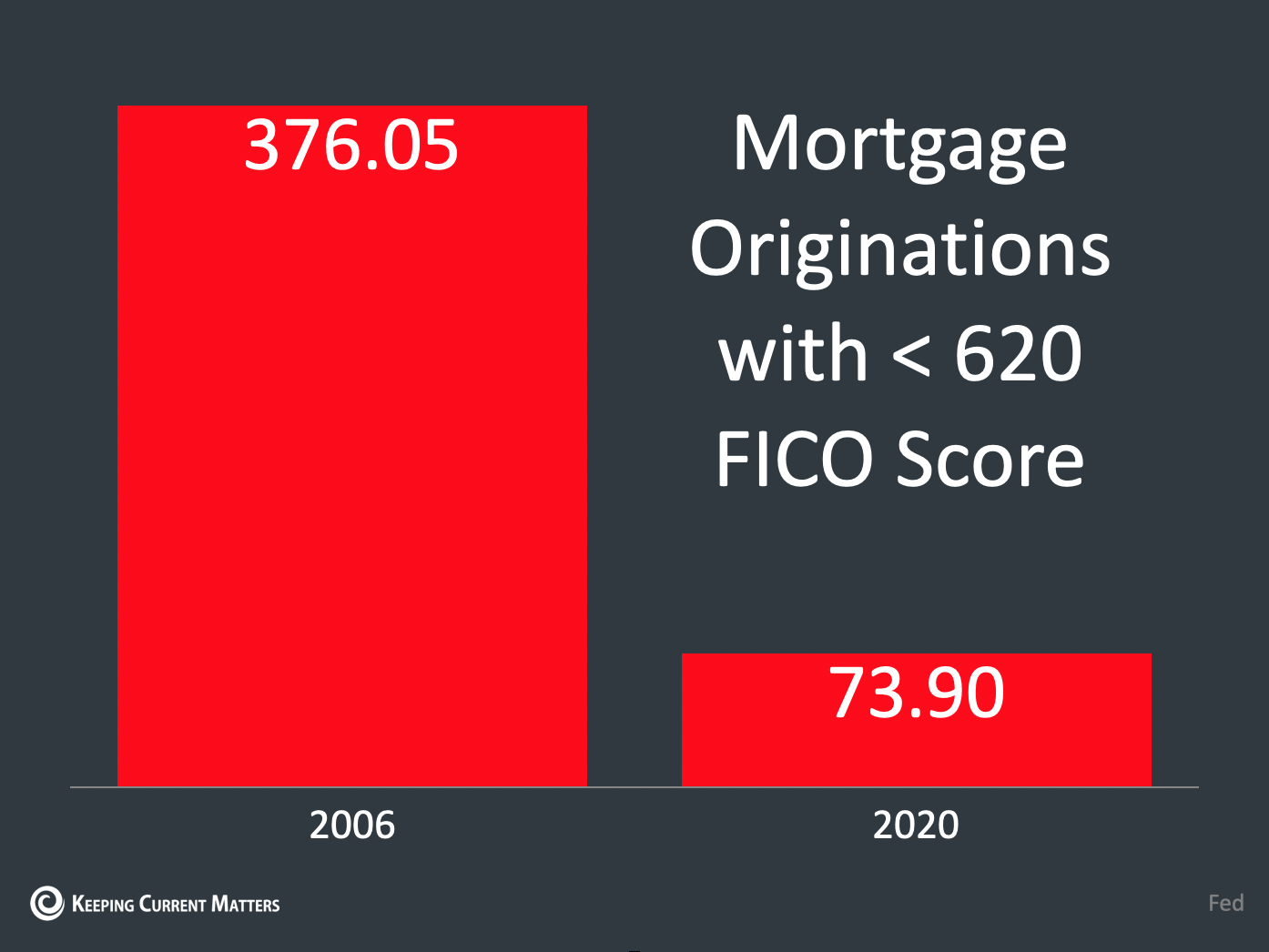

- Unlike lending practices leading up the last housing crash which didn’t require any proof of income, a job, or assets, the number of risky mortgages out there right now is very low. In general since the last housing crash, mortgage rules have tightened so much that only very well qualified buyers could get approved for mortgage over the last 15 years and the amount they qualified for is actually in-line with what they can afford on a monthly bases. Foreclosure rates even before Covid-19 were low due to properly qualified homeowners and this hasn’t changed.

- I talked about Federal assistance programs that have been rolled out to support home owners and keep them from having to go through foreclosure in my July market update but more federal help on top of the already significant spending was just recently announced. For federally backed mortgages, buyers have the option of adding their missed payments onto the end of their loan for no additional costs. This will extend how long it takes them to fully pay off their mortgage however it will keep them from having to sell their home. On top of that they also just announced that if the homeowner isn’t yet financially able to cover 100% of their current mortgage payment, they can restructure their loan to drop the monthly principle and interest payment by as much as 25% to help keep people in their homes and out of the foreclosure process.

As you can see homeowners are in a much better financial position and the government really doesn’t want a repeat of what happened last time so they are doing everything they can to reduce the number of homeowners that have to eventually sell. However there will still be foreclosures so what will those do the housing market when they start to take place at the end of this year and throughout 2022? Let’s look at some more data!

Right now, according to The National Association of Realtors we have about 1.37 million active homes on the market. When we look at that compared to the average number of homes that have typically been on the market at any given time over the past 40 years, which is about 2.5 million, you can see that the supply shortage that everyone is taking about is real. The reason I bring up these numbers is to show you that even if we end up on the higher end or exceed the estimated foreclosure numbers, there is such a supply shortage that is will quickly be absorbed by the buyers out there desperately trying to get into a home right now. Even if we triple the number of homes experts believe will eventually end up in foreclosures we still aren’t even at the normal range for active homes in the typical market and demand right now is much higher than a typical market due to the historically low interest rates.

National numbers are great but what about Orange County specifically? Right now we currently have about 2,537 active homes on the market, when we look back at July from years 2015-2019 we had an average of 6,916 active homes on the market, that is 173% more than today. Can you guess how many homes we had on the market leading up to the last housing crash? (If you follow me in Instagram you probably already know the answer to this) Is it 8,000? 12,000? It was actually right around 16,000! We would need such a giant wave of inventory to hit the market to just get us back to “normal” that it really is hard to imagine how we could realistically get to a point where you start seeing home values drop anytime soon.

So everything is sunshine and rainbows then in the housing market right? Well, there is one concern that I have and in my opinion will be the only thing that can stop home values going up and that is interest rates. They have been so low for the last year and a half, that people could borrow money cheaper than ever before, which means they could afford homes they might not have been able to just 2 or 3 years ago. Besides historic low inventory, low interest rates have been the other main contributing factor to the rapid appreciation we have seen over the last 18 months. People are stretching themselves to take advantage the low rates while they are still here. My concern is that as prices continue to climb, it is making any change in interest rates in the future more and more likely to quickly slow down the housing market because buyers will become more and more sensitive to any rate adjustments. I actually believe that we need higher interest rates right now to help get us back to a more healthy housing market because the supply issue isn’t going to go away anytime soon. If we don’t start seeing higher rates during this last half of the year, we could get to a point in 2022 that buyers are so rate sensitive that even a half a percent jump could slow the market down significantly. I still don’t think we will see depreciation of homes but it could lead to a period of price stagnation for the housing market, which actually might be a good thing for the overall future of the market to make sure we don’t get overheated.

I don’t like projecting that far out because as we all know especially after last year, anything can happen but at the same time I want to make sure everyone is aware of what to watch out for as we go through the back half of this year leading into 2022 so you have a better idea of what might be coming.

Buyers:

My advice for buyers still remains the same, look at what you can afford now and buy for the long term (5+ years) and that will not only give you a stable monthly payment for the next 30 years to help you better financially plan, but over time home values will continue to rise helping you to create some wealth at the same time. Remember, rising interest rates will impact your monthly payments more than the appreciation we are seeing on a monthly bases, and interest rates are at one of the lowest points they have even been for a mortgage. After reading this, if you are still in the camp of, “I’m going to wait for home prices to fall before buying” remember that the most logical reason for home prices to fall right now would be higher interest rates. If rates go up and home prices go down you will still be paying the same amount or even more for a less expensive house in the future. Just a quick example of this to demonstrate my point. Let’s say right now you buy a home that is worth $750,000 and put 10% down with a 3% interest rate, your monthly principle and interest payment would be right around $2,846. Now let’s say next year that same home somehow loses half of the 17% appreciation(the average in OC) it gained over the last 12 months which would be 8.5% or a new price of $686,250. You put the same 10% down but rates go up as expected to around 3.8%, you're now paying $2,878, more than you would have if you bought it at the higher price with the lower interest rate. If you can afford to buy now and are just waiting to see what happens the odds are not in your favor right now. There are still deals out there right now and having an experienced agent to make sure you don’t end up overpaying for a home is key. Your agent should be pointing out what upgrades and features are worth paying a little extra for that add value to the home and what updates are really not helping you out financially even though they may look nice. Make sure you aren’t working with an agent that is just opening the door for you, you need someone that will take the time and give you honest feedback on the home so you can make the best financial decision possible.

Sellers:

I told you last month that if you are looking to sell and find a new property to buy at the same time you probably want to get it on the market asap to take advantage of not only the low interest rates and increasing supply on the buying side, but the steady stream of demand that is currently out there right now on the selling side. I also said that if you aren’t planning on buying a new place with the proceeds of your current homes’ sale you could wait a month or two before selling and demand would still be high. Well, the sudden drop in interest rates has kept demand high and we are now approaching the end of the Summer market for homes and will be moving into the Fall market where demand traditionally slows down. If you are a seller of any type wether you’re looking to buy a new home or not we are down a few weeks before kids start going back to school again which is traditionally when the buyer demand gradually fades. This years Fall market will be busier than usual as long as interest rate remain relatively low but as each month goes on you’ll have less buyers out there shopping compared to today so take advantage of the higher demand created by this temporary drop in interest rates we have seen over the last month while you still can.