Are we Headed for AnotherHousing Market Bubble?

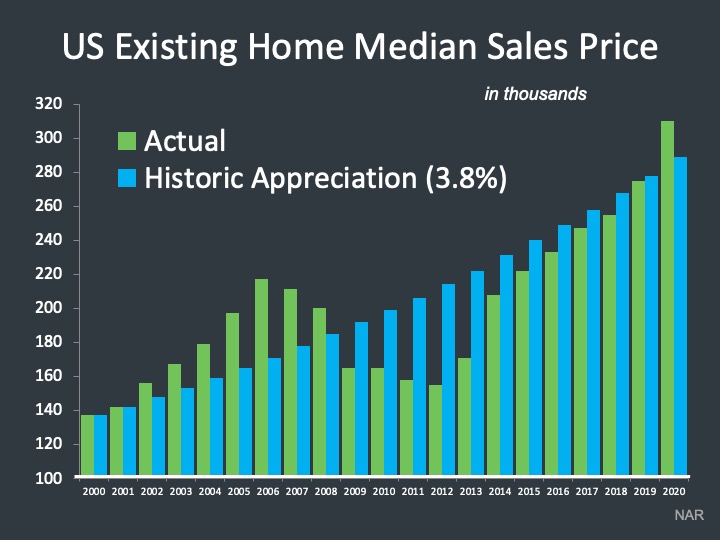

While the average annual appreciation for homes in the US is about 3.8%, we ended 2020 at around 10%. If this type of appreciation continues for another few years, we’ll be at risk of approaching bubble territory. However, one year of rapid appreciation is not likely to impact the housing market significantly, especially when you consider that over the last 11 years, we’ve actually been trending under the 3.8% average as we recovered from the Great Recession. If you look at the appreciation that lead to the last housing crash, you can see that we had years of higher than normal appreciation before everything fell apart.

On top of that the housing market fundamentals are completely different this time around, loans are more secure, homeowners have a lot of equity in their homes, inventory is significantly lower than it was before they last crash, I could go on and on but I’ll save comparing the two in more detail for another day.

So are we are the beginning of the next giant bubble?

The good news is that what happened last year in terms of appreciation will most likely not happen again this year, or in the years to come. Here are the reasons why:

Inventory should start to increase at a quicker than normal pace

- The typical housing cycle is about to begin: I know it’s still February, but the early signs of the Spring market are starting to appear. Like most years, we will start to see sellers placing their homes on the market in larger numbers, especially when we get into March. Month-by-month inventory will hit the market faster and faster until the number of homes hitting the market per month peaks, typically around May. However, because of the delayed start to the supply rising, I wouldn’t be surprised if that peak happens a month or two later this year.

- COVID-19: Last year, COVID was one of the reasons many homeowners who might have had plans to sell put everything on hold because of uncertainty in the economy, fear of contracting COVID, and/or job loss. This year as the vaccines continue to roll out faster and faster, as confidence in the economy is grows again, and as employment rates return to normal, many of these homeowners are expected to restart their plans to sell.

- Foreclosures: While we never want to see anyone lose their home, we have to acknowledge the reality that foreclosures will start to pick up this year. However, unlike some of the headlines you might have read in the news, we are very unlikely to see a “wave” of foreclosures hitting the market all at once – for many reasons, but here are a few:

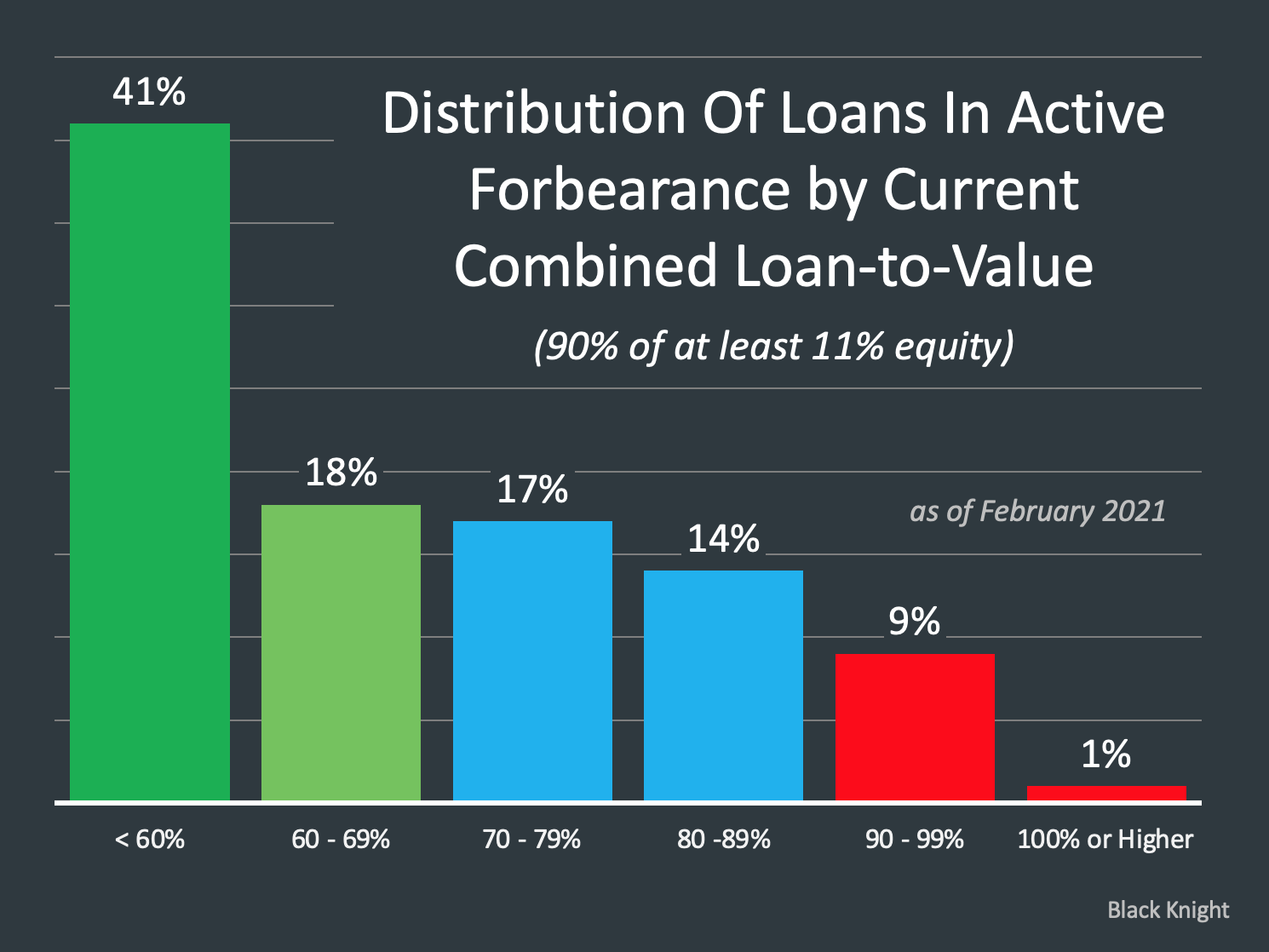

- 90% of home owners in forbearance currently have more than 10% equity in their home. This means that if they were looking at going into foreclosure, they would end up just listing their home on the market as a normal sale beforehand, and because demand is so high right now, those homes would be quickly absorbed by the market, selling for market value, allowing those owners to exit their homes and at minimum, breaking even – but in the large majority of cases, making a profit.

- Foreclosures take time – sometimes up to a year or more – so we are not going to have a giant wave of foreclosures hitting the market all at once. Plus, the government has continued to extended the forbearance periods for many mortgages (now through June). So although we’ll see an uptick of foreclosures this year, they will be spread out starting in the Summer and going though all of next year.

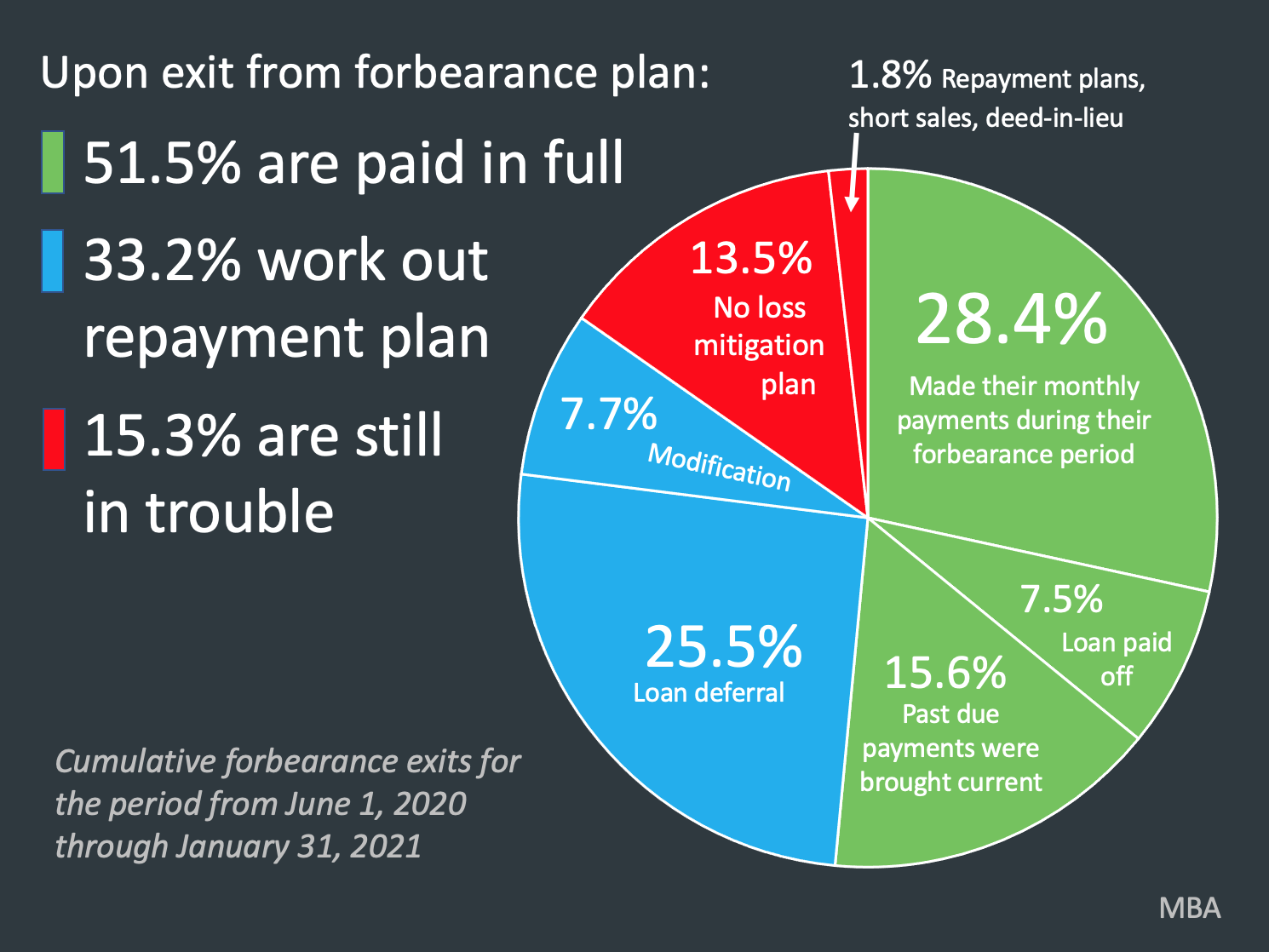

- The overwhelming majority of those who have exited forbearance (so far about 85%) have either paid their mortgage off in full, caught up on payments, or negotiated with their bank to modify their mortgage.

This number will rise as more distressed homeowners – those who have needed to stay in forbearance long-term – start to exit, but even if the number goes higher, experts are predicting the market will be able to absorb the additional inventory.

This number will rise as more distressed homeowners – those who have needed to stay in forbearance long-term – start to exit, but even if the number goes higher, experts are predicting the market will be able to absorb the additional inventory. - Over the last three years, the average number of foreclosures to hit the market in the U.S. has been about 290,000. The current number of homeowners in forbearance is 2.7 million, so even if 10% of those owners end up exhausting all options and are forced to sell, it would be result in fewer foreclosures than in a normal year. Also, remember that we started off the year with 430,000 fewer homes on the market nation wide and demand is stronger than last year as well. Another thing to keep in mind: even if we do see a larger than expected number of foreclosures hit that market in the next 2 years, the demand side of the housing market has an ace up its sleeve: Millennials. Between the years 2020-2024, the largest demographic patch in the country is now reaching peak home-buying age. Millennials have delayed buying houses for longer than the generations before them, but they’re now in the prime years to purchase their first home. And those Millennials who did buy early will be looking to move up to a larger home as their families grow. This extra demand over the next few years could help with more unexpected jumps in inventory and help keep the housing market healthy for the foreseeable future.

- 90% of home owners in forbearance currently have more than 10% equity in their home. This means that if they were looking at going into foreclosure, they would end up just listing their home on the market as a normal sale beforehand, and because demand is so high right now, those homes would be quickly absorbed by the market, selling for market value, allowing those owners to exit their homes and at minimum, breaking even – but in the large majority of cases, making a profit.

As the economy improves, interest rates are projected to rise

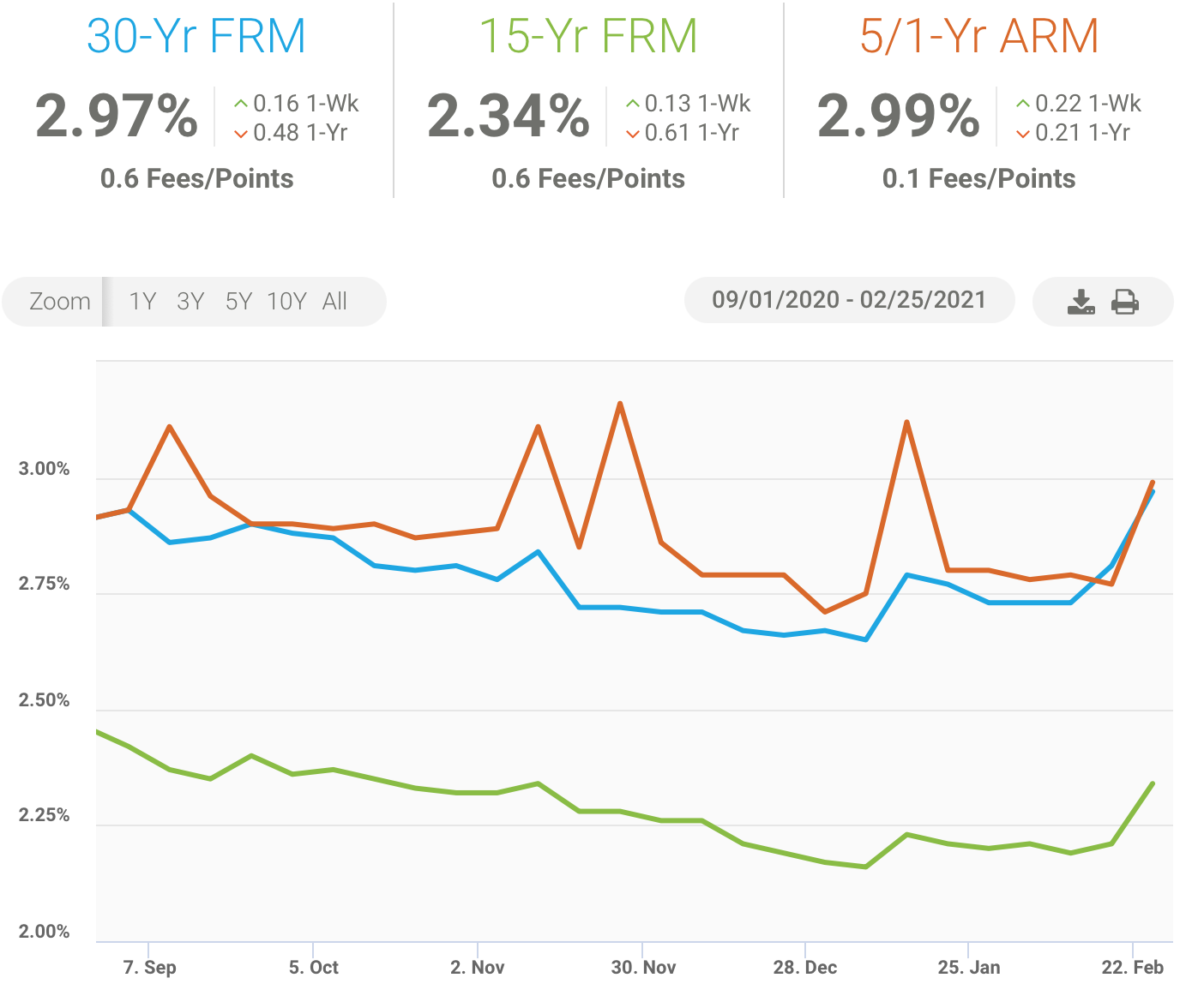

Thirty year fixed rate mortgages hit new all time lows more than a dozen times last year but these extremely low interest rates are about to start climbing – and, in fact, they already have. We started the year at an average of 2.65% and, as of today, we’re sitting at 2.97%.

As the year goes on, the economy will continue to improve and people will get back to work. Because interest rates tend to reflect the confidence in the economy, nearly all experts are predicting they will continue to rise as long as there isn’t another major set back involving COVID-19.

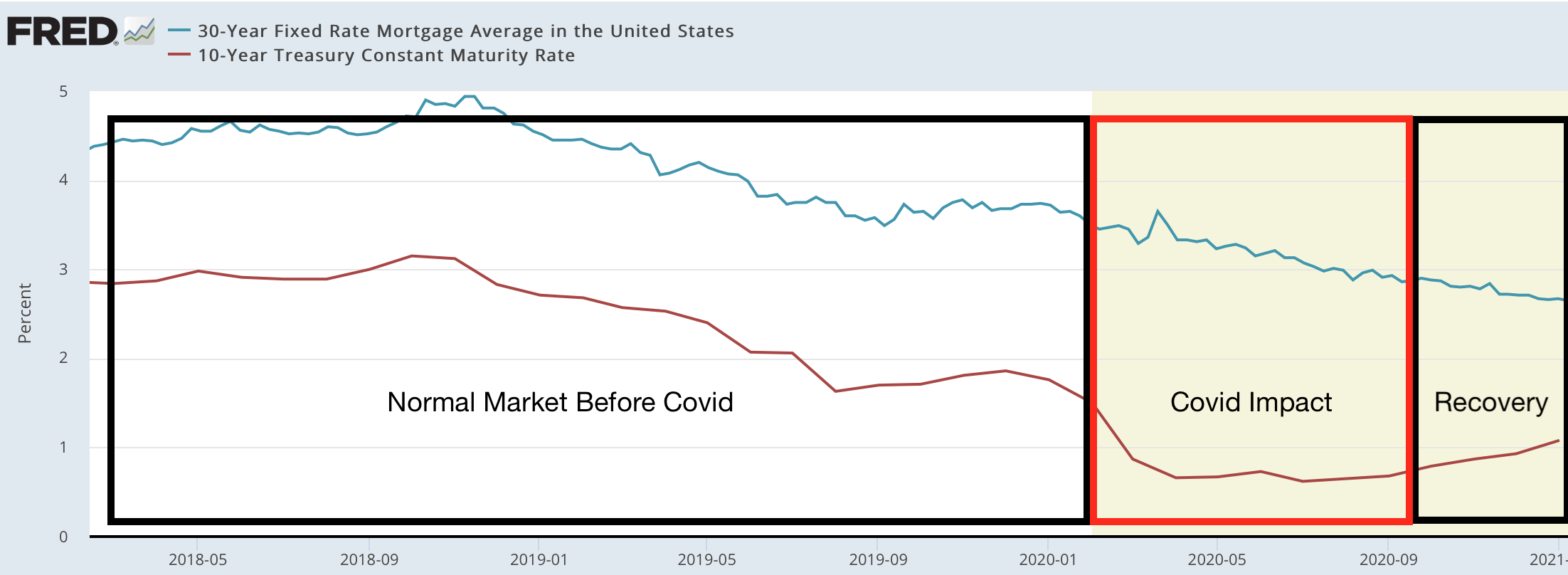

Another key indicator that interest rates will continue to climb is the 10-year treasury bond. But why is that?

The answer: Rates for a 30-year fixed mortgage loan most closely track with what the 10-year treasury bonds are doing, making them one of the most widely tracked and cited bonds in the mortgage world. The stronger the economic outlook, the higher the 10-year treasury bonds tend to go, and this year, the 10-year treasury bond has been on the rise.

The 10-year bond initially dropped from about 1.8% to 0.6% from the beginning of 2020 to when the first COVID-related shut downs started. It didn’t get back above 1% again until the very beginning of 2021. Since then, it’s been on the rise. In January, it went to 1.1%. Last week it was at 1.2%, and this week they are now at 1.49%.

The typical spread between the 10-year treasury bonds and 30-year fixed mortgages runs somewhere between 1.5%-2%. So, as an example, if the treasury bond was sitting around 1.5%, then you would expect mortgage rates to be somewhere between 3%-3.5%. However, during the pandemic, the difference between the two rose to as high as a 2.7% – way above average – but since then, the spread has now come back to being within that 1.5%-2% range, which tells me that the 10-year treasury rates will again start to have a more predictable impact on mortgage rates going forward.

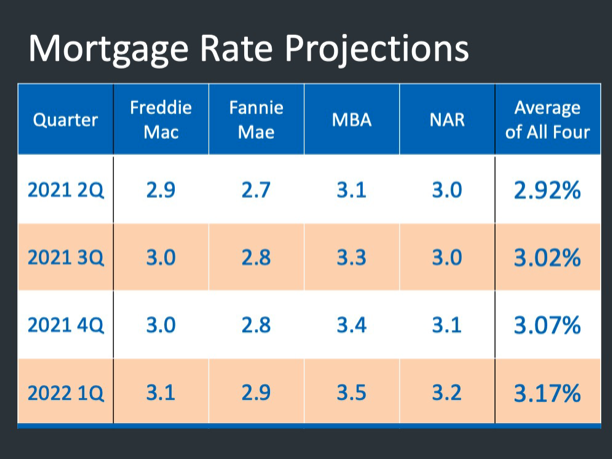

Based on economic projections as well as what the Fed is saying about what they are planning to do with interest rates, most experts expect that interest rates will climb to somewhere between 3%-3.5% by the end of the year.

This might not seem like a significant difference (especially considering that if they stay below 3.5%, they would still be some of the lowest rates historically that we have ever seen) but keep in mind that every time interest rates go up, even by as little as a tenth of a point, buyers can afford less. So every time they increase, there will be some buyers dropping out of the market, especially if they go to the higher end of projections.

Between the normal Spring and Summer market cycle, pent up supply that didn’t hit that market last year, and some foreclosures, inventory should hopefully start to increase fast enough to help buyers who have been struggling with so much competition over the last year to at least come up for a breath of air. At the same time, interest rates should gradually climb, and this will naturally slightly shrink demand. However, because we have such a historic, once-in-a-generation gap between supply and demand in the housing market right now, the market is going to be able to absorb homes pretty easily while still keeping us in a seller’s market.

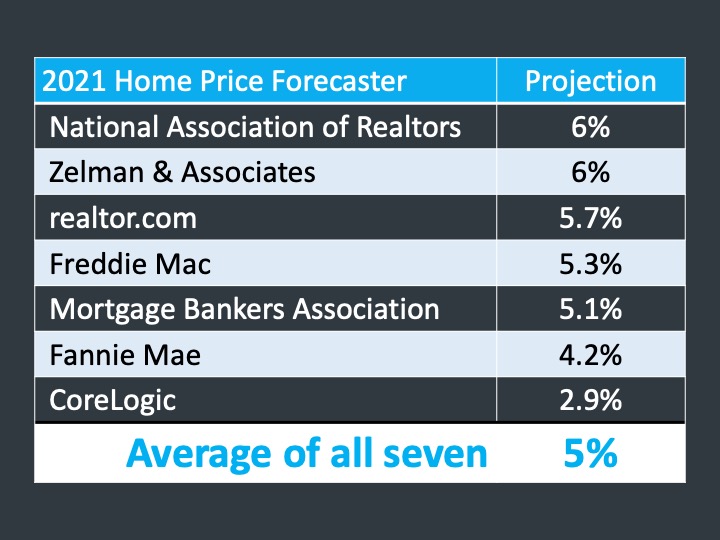

Also, because demand usually peaks at the beginning of Summer, I expect appreciation to cool down more dramatically during the second half of the year. Most experts are predicting somewhere around a 5% increase in home values this year. I think that in Southern California, you will probably see a little higher than that, especially in Riverside and San Bernardino.

The majority of the appreciation will probably happen before June of this year and as demand starts to decrease, as it usually does in mid-Summer through the rest of the year, appreciation will slow. It’s still projected to be a seller’s market for the remainder of the year, but instead of being in an unsustainable overheated seller’s market, we will likely transition back to a hot seller’s market that will be better for the long term health of the housing market and keep us from entering into a new housing bubble.

I’ll end by saying that even with market forces naturally bringing some balance to the housing market, I don’t see us being able to claw ourselves out of the lowest supply of homes the U.S. has seen since 1981 – especially far enough that appreciation stops or even goes down.

This means it’s important for buyers to know that the same advice I have been giving for the last 10 months still applies: Continue trying to buy now even though there will be more competition for a home. The longer you wait, the more homes will appreciate and the higher interest rates are expected to climb this year. Buy for the long term (5+ years), focus on the monthly payment, and if you can find a place to call home, you will be able to lock in a 30-year mortgage at one of the lowest rates we have ever seen.

Sellers, now is also the time to get your home on the market before the number of homes for sale starts to increase at a quicker pace in about a month. The market should be on your side for the remainder of the year, but your advantage will slowly dissipate as the months go on.